経済財政諮問会議 2026年3月26日

2026-03-26一次資料(出典)

議事録・配布資料の全文(政府公表資料より。要約でなく原文に基づく参照用)。

議事録

令和8年第3回経済財政諮問会議

議事要旨

―――――――――――――――――――――――――――――――――――――――――――

(開催要領)

1.開催日時:令和8年3月 26 日(木)18:02~18:46

2.場

所:総理大臣官邸4階大会議室

3.出席議員:

議長

高 市

早 苗

内閣総理大臣

議員

木 原

稔

内閣官房長官

同

城 内

実

内閣府特命担当大臣(経済財政政策)

同

林

芳 正

総務大臣

同

赤 澤

亮 正

経済産業大臣

同

片 山

さつき

財務大臣

同

植 田

和 男

日本銀行総裁

同

筒 井

義 信

日本生命保険相互会社 特別顧問

同

永 濱

利 廣

株式会社第一生命経済研究所 首席エコノミスト

同

南 場

智 子

株式会社ディー・エヌ・エー 代表取締役会長

同

若田部 昌 澄

早稲田大学政治経済学術院教授

4.有識者:

オリヴィエ・ブランシャール

ケネス・ロゴフ

マサチューセッツ工科大学名誉教授

ハーバード大学教授

(議事次第)

1.開 会

2.議

事

(1)特別セッション

3.閉

会

(資料)

資料1-1

資料1-2

資料2-1

資料2-2

オリヴィエ・ブランシャール氏提出資料(英語)

オリヴィエ・ブランシャール氏提出資料(事務局による日本語訳)

ケネス・ロゴフ氏提出資料(英語)

ケネス・ロゴフ氏提出資料(事務局による日本語訳)

配付資料1-1 現時点における高市政権の取り組み(内閣府)

配付資料1-2 現時点における高市政権の取り組み(内閣府)(事務局による英語訳)

1

令和8年第3回経済財政諮問会議

※ブランシャール氏、ロゴフ氏の発言は内閣府による仮訳。

※ブランシャール氏、ロゴフ氏の発言要旨は本人に了解いただき、別途掲載。

(概要)

(城内議員)

ただ今から「経済財政諮問会議」を開催する。

〇「特別セッション」

(城内議員) それでは、まずは高市総理からご発言をいただく。

(高市議長) 本日は、我が国の経済財政運営について、海外有識者との対話を通じ

て、国際的な議論の中に位置づける「特別セッション」を開催する。

今回、世界的に著名なマクロ経済学者の有識者として、米国からオリヴィエ・ブラン

シャール教授、そして、ケネス・ロゴフ教授のお二人にご参加をいただいている。

大変ご多用の中、本セッションに参加いただき、心より感謝を申し上げる。

日本は、「技術革新力」や「労働の効率性」などの面では他国と遜色がないにもかか

わらず、国内投資が圧倒的に不足して、潜在成長率が低迷している。このため、高市内

閣は、「責任ある積極財政」の下、官民協調で国内投資を大胆に促進し、雇用・所得・

生産性を引き上げる方針を打ち出した。特に、経済安全保障などの「危機管理投資」、

AI・半導体などの「成長投資」が鍵になると考えており、戦略分野の「官民投資ロー

ドマップ」の策定を進めている。

こうした「戦略的な財政出動」を進める中で、政府債務残高対GDP比を安定的に引

き下げることにより、財政の「持続可能性」を実現し、「市場の信認」を確保していく

方針である。

本日の会合では、「世界経済に関する分析」や、直面する課題に応じた「マクロ経済

政策の在り方」についてご意見を伺うとともに、日本が進めている経済財政運営の方向

性についても忌憚のないご意見をいただきたいと考えている。どうかよろしくお願いす

る。

(城内議員) 続いて、ブランシャール教授から一言ご挨拶をお願いする。

(ブランシャール氏) ありがとうございます。まず、先日の選挙結果について心より

お祝い申し上げる。また、私とロゴフ教授を招き、日本の財政政策について議論する機

会を設けてくださったことに、深く感謝する。簡単に自己紹介をさせていただく。私は

マクロ経済学者である。キャリアの大半はMITの経済学部教授として過ごしてきた。

2008 年から 2015 年まではIMFでチーフエコノミストを務めていたが、これはロゴフ

教授とも共通している。この数年、私の主たる関心は財政政策の設計にある。よって、

今回こうして皆様と直接議論し、学ぶ機会を得られたことを大変うれしく思っている。

現在の日本の状況において、財政政策には二つの目標が必要だと考えている。

第一は、総理もおっしゃったように、政府債務残高対GDP比を安定させることであ

る。現時点では、金利と経済成長率の組み合わせから見て、これは比較的容易である。

しかし将来的には、より難しくなることは明らかである。金利と経済成長率の差は縮小

していくだろう。この点について考えておく必要がある。その意味するところは、おそ

らく、そう遠くない将来のある時点でプライマリーバランスの均衡を目指す必要がある

ということである。

2

令和8年第3回経済財政諮問会議

第二の目標は公的な投資を守ることである。これは総理の冒頭のご発言にもあった点

である。このためにはプライマリーバランスの均衡に向けた調整ペースを緩める必要が

あるかもしれない。しかし、その場合でも、そう遠くない将来のある時点でプライマリ

ーバランスの均衡を達成するという基本的な方向性自体は維持されなければならない。

この二つの目標は、信頼できる中期的な財政計画の中で組み合わせていくべきであ

る。そして、日本がこれまで財政目標の達成に苦労してきたことを踏まえると、信認の

確保が極めて重要である。その信認を生み出すために、どのような制度が必要かを考え

なければならない。ありがとうございます。

(城内議員) ロゴフ教授からご挨拶をお願いする。

(ロゴフ氏) 私もまた、この会合を開催してくださった総理に感謝申し上げるととも

に、日本の成長と繁栄を力強く後押ししようとする取組を称賛したいと思う。そして、

私とブランシャール教授を招いてこの会合を開かれたこと自体が、それを責任ある思慮

深い形で進めようとする総理のコミットメントの一つの表れだと受け止めている。私は

マクロ経済学者として、金利、為替レート、中央銀行の独立性、さらに債務や金融危機

といったテーマを研究してきた。

本日は、様々な理由から世界全体が共有している金利上昇環境下での課題についてお

話ししたいと思う。その理由の一つは、日本だけでなく世界中で債務水準が高いことで

ある。もう一つの理由は、もちろんながら、軍事支出への圧力が突如として高まり、そ

れが金利に上昇圧力となっている世界情勢にある。ポピュリズム、貿易の分断、AI投

資支出も挙げられる。日本も、こうした圧力から免れてはいない。

経済学者がスタグフレーションショックと呼ぶ、成長を押し下げつつインフレを押し

上げる現象に直面する中、高債務と高金利が同時に存在する中で政策運営を行うことは

とりわけ困難なものになっている。率直に言えば、現在進行中のショックは、この50年

で最大のものになりつつある。イラン戦争が、関税戦争、ウクライナ戦争、その他の要

因の上に重なり、長期的な影響を及ぼす可能性が高いからである。この種のショック

は、通常の需要ショックよりはるかに対処が難しいものである。究極的には、総理が目

指しておられるように、成長を活性化することが唯一の道である。総理と閣僚の皆様が

そのためにどのようなお考えをお持ちか、伺うのを楽しみにしている。ありがとうござ

います。

(城内議員) プレスはご退室をお願いする。

(報道関係者退室)

(城内議員) ブランシャール教授から、資料1に基づきご説明をお願いする。

(ブランシャール氏) 四つの点を手短に申し上げる。主なメッセージは、先ほど報道

陣の前で述べたことを、少し違う形で言い直すものである。

第一に、日本では債務比率の水準が明らかに非常に高いわけだが、それ自体が大きな

問題というわけではない。60%や 90%といった危険水準があるわけではない。ただし、

それが大問題でないとしても、債務水準が高いことによってリスクにさらされやすくな

るのは事実である。たとえば、金利の変動が予算に与える影響が大きくなり、より大き

な調整が必要になるからだ。したがって、他の条件が同じであれば、債務水準は低い方

が望ましいのは明らかである。しかし、それが絶対的な優先事項というわけではない。

3

令和8年第3回経済財政諮問会議

本質的に重要なのは、債務比率が制御不能な形で持続的に上昇しているという印象を

与えないことだ。これが投資家の気にする点である。債務比率が安定していれば投資家

はそれを受け入れる。しかし、政府がコントロールを失ったと感じられれば、いわゆる

負の連鎖が生じ、金利上昇がさらなる悪循環を招くことになる。したがって、日本の文

脈では、最低限、債務比率を安定させ、できれば時間をかけて徐々に引き下げていくた

めの、明確で信頼できる計画を持つことが重要である。ここでのポイントは、債務比率

の安定化が目標として極めて重要だということだ。

次の点は、債務比率の動学に関するもので、これは皆様にもお馴染みの内容である。

債務比率の推移は二つの要素によって決まる。金利と経済成長率の関係、そして、プラ

イマリーバランスだ。現在の状況では、ご存じのとおり、既発債に対する金利が経済成

長率を下回っているという意味で、ある意味では恵まれた状況にある。そのため、それ

だけでも債務比率は低下する傾向にある。しかし、ロゴフ教授もこのあと強調されると

思うが、また、皆様もよくご存じのとおり、これは永続しない。極めて低い、あるいは

マイナスの金利のもとで発行された国債が多くあるが、そうした環境はいずれ終わって

いく。そして、世界全体として見れば、いわゆる中立金利は今後より高くなる可能性が

高いと思う。

したがって、将来のある時点、たとえば5年後には、金利と経済成長率が等しくなる

という前提を置く必要がある。そうなると、算術的な帰結として、5年後の時点で求め

られるのは、プライマリーバランスをゼロにすることである。これが債務比率を安定さ

せるための条件である。では、どれくらいのスピードで行うべきか。私は5年という例

を置いている。なぜなら、1年で達成しようとすれば需要に壊滅的な影響が出ることは

明らかだからである。または、10 年かけて達成する、あるいはそう装うだけでは誰も納

得しないからである。その中間に適切な期間があるはずだ。私は4~5年程度が妥当な

前提だと思う。したがって、実務的には、5年後のプライマリーバランスを一つの基準

として考えるべきだろう。私には、それが適切な時間軸に思われる。

次の点は信認についてである。政府が約束をして、それを果たさない例は誰もが耳に

したことがあるだろう。したがって必要なのは、信頼できる複数年の計画である。その

ためには二つ必要である。第一に、債務の推移を予測するツールである。不確実性や、

たとえば年金制度に由来するもののような暗黙の負債も考慮に入れるものだ。専門的な

名称として、SDSA(Stochastic Debt Sustainability Analysis、確率的債務持続可

能性分析)と呼ばれる。しかし、その本質は、何が起こる可能性があるのか理解し、

様々な政策がどのような効果を持ち得るのかを評価することにある。これは開発すべき

不可欠なツールだと考えている。

第二に、そのツール自体と、そのツールを用いて得られる結論自体が信頼できるもの

でなければならない。そのためには、独立した機関、いわば監視機関によって行われる

必要があると思う。つまり、「はい、今後は事態はこのようになる可能性が高い」と言

える機関だ。内部で行われたものについては、投資家は懐疑的になりがちである。した

がって、その監視機関と、たとえば財務省との間には一定の距離があることが重要であ

る。

最後に、投資を保護する必要性に照らして極めて重要な点について申し上げる。経済

学者として私が言いたいのは、投資だからといって自動的に国債を財源としてよいわけ

ではないということ。民間企業の場合のように、投資そのものを正当化する財政的収益

4

令和8年第3回経済財政諮問会議

が見込めるのであれば、そうすることも可能だろう。しかし、皆様が行う、いわゆる

「危機管理投資」は、私も重要性が高いと考えているが、おそらく明確な財政的収益が

見込めるとは言いにくい。財政的収益があるかもしれないし、そうでないかもしれな

い。成長を押し上げるかもしれないし、そうでないかもしれない。それだけを根拠に国

債を財源とすることを正当化することはできない。したがって、可能であれば、こうし

た投資はかなりの部分を税を財源とすることを試みるべきであると考える。

もっとも、政治的制約を考えれば、皆様が考えている公的な投資は部分的には財政赤

字を活用せざるを得ない。したがって、私が先ほど述べた調整の道筋は、最終的に5年

後にはプライマリーバランスがゼロになるという点についての信認が保たれる限り、や

や緩やかなものになり得る。私は、公的な投資についてはそのように考えるべきだと思

う。

(城内議員) それでは、ロゴフ教授にお願いする。

(ロゴフ氏) ありがとうございます。まず最初に、大学の教授会に関する有名なジョ

ークを引用したいと思う。「言うべきことはすべて言われたが、まだ全員が言ってはい

ない」。今の私の立場は、まさにそれに少し近いものである。ブランシャール教授が非

常に優れた発言をされたので、私のスライドも似た領域を扱っているが、少し異なる点

を強調したいと思う。

私たちは、ほんの数年前とは全く異なる世界に生きている。それにもかかわらず、有

権者の感覚も政治家の感覚も、まだ金利は安定的に極めて低いという世界に合わせたま

まである。日本はその恩恵をより長く享受してきたが、私もブランシャール教授と同

様、低金利は永遠ではないと考えている。実際に、長期実質金利が上方に回帰する可能

性は、私がこの 10 年間研究してきた大きなテーマだ。その意味で、日本の長期国債の金

利が今後数年で3%、あるいはそれ以上に上昇しても、私は全く驚かない。現在円が非

常に弱いという事実は、日本が世界の金利動向に十分には追いついていないことを部分

的に反映していると思う。

こうした変化にはいくつも背景がある。一つには単純に、世界中で債務がますます増

え続けていること。もう一つには、政治が変わったこと。財政赤字による支出を使うべ

き、ワシントン・コンセンサスを放棄すべきだという圧力が以前より遥かに強まってい

る。加えて、貿易システムの分断も金利上昇圧力になる。そして何より、世界中で軍事

支出が今後長年にわたり劇的に増加していく世界を私は予想している。私の母国である

米国では、軍事支出は冷戦終結時の半分まで落ちたが、その状態が続くとは思えない。

欧州から中国、日本に至るまで、世界中で同様の支出圧力がなお高まり続けているのが

分かる。さらに、AIデータセンターやそれに伴う電力需要からも上昇圧力が生じてい

る。確かに、人口動態のように金利を下押しする要因もまだ存在している。しかし、非

常に長い期間にわたり、全体としては上昇方向への圧力が強まると私は考えている。金

利は何世紀にもわたって低下してきたというのは確かだが、この 100 年を見ると必ずし

もそうではない。

そこで問題となるのは、日本に何ができるのかということだ。私は、日本には本当に

たくさんの強みがあると思っている。たとえば、テクノロジーやロボティクスの分野で

ある。総理が冒頭発言で的確に指摘されたように、日本は多くの分野で最先端にいる一

方で、投資が不足している。公的な投資やインフラの維持、民間部門の活性化といった

余地が残っていると思う。もっとも、それにも限界がある。ブランシャール教授も穏や

5

令和8年第3回経済財政諮問会議

かな形で述べていたが、政府による投資であること自体が、その効果を自動的に保証す

るわけではない。

幸い、日本の大企業は驚くほど効率的である。世界的に見ても依然として非常に成功

しており、特にグローバルサプライチェーンの高付加価値ニッチ市場にうまく入り込む

ことで世界的にも引き続き高い競争力を維持しており、それが、日本をなお世界第4位

の経済大国たらしめている理由である。したがって、投資をどの分野で、どのような形

で後押ししていくかを、よく見極める必要がある。

制度面について言えば、ブランシャール教授が言及した財政機関は、独立した見通し

を作るための非常に良い考えだと思う。万能ではないが、検討する価値は十分ある。

しかし、それ以上に重要なのは中央銀行の独立性である。政府が金利を押し上げるよ

うな政策(巨額の財政赤字)を講じている、あるいは、世界的な金利上昇が生じている

ことを受け入れざるを得ないと市場が懸念するまさにその時に、中央銀行が政府に強く

従属していると見なされると、非常に問題が生じかねない。それは、さらに長期金利を

押し上げる要因となりかねない。

最後に申し上げたいのは、私たちはより劇的で、より不安定な世界に生きているとい

うこと。1年前の世界とも違うし、まして5年前の世界とも違う。中国の重要性が高ま

り、欧州や世界の金融システムの構図、そしてドル覇権が揺らぐ中で、日本がどう対応

していくかは、日本が直面する金融面の大きな課題の一つだと見ている。日本はこのこ

とにも対応していかねばならない。ありがとうございました。

(城内議員) 高市総理からご質問をお願いする。

(高市議長) それでは、ロゴフ教授に質問をさせていただく。

高市政権としては、財政の「持続可能性」と、必要な投資を含めた財政の「機動性」

を両立させるための取組に着手をしている。

その際、経済財政運営を行う我々政策担当者が、財政の持続可能性に関する「シグナ

ル」として、あらかじめ留意しておくべきマーケットが意識する「メルクマール」とは

何だとお考えかということを伺いたい。

続けて、ブランシャール教授にも伺う。

今様々ご提案をいただいたが、その取組を進めていく際に、「マーケットとの対話」

を通じて、市場関係者にその趣旨を正しく理解してもらうために気をつけるべき点につ

いてアドバイスをいただきたい。

(城内議員) 民間議員からもお一人ずつご発言をいただきたい。

(筒井議員) まず、ブランシャール教授にお伺いする。

ご提案の中で、最低限の目標として、名目債務の伸びを名目GDPの伸びと同程度と

する、そして、複数年計画、中期、5年程度とおっしゃったが、プライマリーバランス

の経路を重視する点についてである。

仮に財政状況が悪化していることが確認された場合は、同時に民間部門の厳しい経営

状況と重なることも多いと思う。そうした場合に備えて、市場の信認を維持するために

どのような経済財政運営のルールが望ましいとお考えか。

ロゴフ教授にお伺いしたい。

金利が高い世界における日本への示唆をいただいた。それは、政府債務残高対GDP

比の低下に向けて、プライマリーバランスの赤字を徐々に均衡に近い水準に保つことが

求められるとのご指摘である。他方で、議論にあるように、防衛関係の能力は一層重要

6

令和8年第3回経済財政諮問会議

性を増してきている。

こうした状況に対応しつつ金利上昇に備えるため、成長促進投資はもちろんである

が、同時に、各方面からの抵抗も予想されるが、既存の歳出の見直しも避けてはならな

い局面も出てくると思われる。この点で、各国での議論あるいは取組で何か参考になる

事例があればご教示をいただきたいと思う。

(永濱議員) まず、ブランシャール教授へ質問する。

日本では、補正予算への依存を減らしていくという方向性にあるのだが、そうなると

自動安定化装置の役割がこれまで以上に重要になると考えられる。教授は、これまで消

費税を自動安定化の仕組みの一部として活用する可能性についても論じられていると思

うのだが、こうした文脈において自動安定化装置の意義をどのようにお考えか、お聞か

せ願えればと思う。

それから、財政を考える際には、総債務で見るべきか、純債務で見るべきかは大きな

論点だと思うのだが、日本のような国では財政の持続可能性や信認を判断する上で、ど

ういった範囲でどの指標を軸に据えるべきだとお考えか。

加えて、日本銀行の当座預金への利払いまで含めて統合政府として捉える見方もある

のだが、その考え方を強く取り過ぎると、中央銀行の独立性との関係が曖昧になるとの

向きもある。そこで、統合政府の見方はどこまで有効で、どこに限界があるとお考え

か。お聞かせ願えればと思う。

それから、ロゴフ教授へのご質問。

日本では、国債が金融システムに深く組み込まれているので、金利上昇は財政と金融

の両面に影響することになっている。ということは、他方で、平時から信認を確保でき

れば、危機対応とか必要な投資に使える余地も確保しやすくなるように思う。

こうした状況を踏まえて、日本が高金利時代になる中でも、危機対応や投資を強化し

て潜在成長率を高める上で、財政も含めてどのような取組を重視すべきだとお考えか。

教えていただければと思う。

(南場議員) まず、ブランシャール教授にお伺いする。

危機の引き金は市場がコントロールを失ったと受け止めたときで、そこに明確な境界

線はないとのご指摘は大変重要と思った。市場の信認は政策当局の意図どおりに得られ

るものではない。そういった観点で、債務残高対GDP比、プライマリーバランス、国

債発行額などの重要指標について、これまでの取組や成果を後戻りさせず、トレンドの

変化や不連続性を生じさせない積み重ねが重要なのではないかと思うが、こういった財

政運営のトラックレコードを積み重ねていくことの重要性をどのようにお考えか。

二つ目の質問は、ブランシャール教授とロゴフ教授、お二人にお伺いする。

現在は、成長率が金利を上回る状況にあるものの、今後その関係が変化していく可能

性とその不確実性に言及されている。このような転換期における経済財政運営におい

て、日本が10年後に振り返ったときにこれだけは注意するべきだったと言われないため

に、リスク管理という点で最も重要なことは何であるとお考えか。

(若田部議員) まず、ブランシャール教授へ質問する。

ブランシャール教授からは、投資の別枠についてお話があったが、投資を通じたGD

Pの成長や税収増への寄与など、定量的なインパクトを経済試算、教授の言葉で言えば

SDSAに取り組み、歳出と歳入を透明化させるという革新的なことに取り組む方向で

日本政府は考えている。こうしたセパレート・インベストメント・アカウントの具体化

7

令和8年第3回経済財政諮問会議

についてはどうお考えかということを伺いたい。

続いて、ロゴフ教授に伺う。

最後のところでもお話があったが、ドル中心の秩序が通貨・金融の仕組みにとどまら

ず、安全保障や海上秩序とも結びついてきた。もしその安定性が弱まるとすれば、日本

のようにエネルギー輸入と海上輸送への依存が大きい国にとって、経済面だけでなく安

全保障面でも重要な含意を持つのではないかと考えられる。日本にとって最大の脆弱性

をどこに見ているのか、また、どのような備えが必要とお考えなのか、よろしくお願い

する。

(城内議員) 海外の有識者のお二人から、総理及び民間議員の皆様の質問にそれぞれ

お答えいただきたい。

(ブランシャール氏) いずれも非常に素晴らしい質問であり、豊かな議論につながり

得るもの。まず、総理のご質問、つまり「どうすれば投資家を納得させられるのか」に

ついてである。繰り返しになるが、投資家が懸念しているのは、事実上のコントロール

喪失、あるいはコミットメントの欠如である。もちろん、これはかなり曖昧な概念であ

り、そうなることもあれば、ならないこともある。しかし、それに対処する方法は、私

が申し上げたとおり、信頼できる複数年計画を持つこと。

そのためには二つのツールが必要である。一つは、その計画がどこへ向かっているの

か、また、おそらく成功し得ることを示すツールだ。もう一つは、その評価が独立機関

によって行われ、基本的に「はい、それでよい」と結論付けるものであること。また、

状況は年々変化する。そのため、毎年この検証をやり直し、「この理由で目標未達だっ

たので、次はこうする」と結論づけるか、ロゴフ教授も述べたように環境が大きく変わ

ったので、それに応じて調整するといったことが必要になる。

それが、非常にオープンで、信頼でき、専門的かつ独立した形で行われるならば、投

資家は受け入れるはずである。それ以上に踏み込み、つまり財政ルールを設けるべきだ

という見方もある。たとえば「プライマリーバランスの赤字がXを超えたらこうする」

「債務がYを超えたらこうする」というものである。しかし、私自身が欧州連合(E

U)の財政ルールに関わった経験から言えば、それはかなり次善的な対応だと思う。自

らが何をしようとしているのかをオープンに示し、数字を見せる方が、時には有用だが

時には非常にコストの高い機械的なルールを持つよりも、良いと思う。そして、そのル

ールのコストが高くなりすぎると、政府は抜け道を探す。ですから、私は財政ルールに

は賛成していない。ただし、これは経済学者の間でもまだ決着していない議論である。

これでいくつかの質問にはお答えできていると思う。補正予算について、「それは追

加でやらなければならないことだ」と聞こえる。よって、SDSAに不確実性や追加支

出の可能性を織り込むことこそが本来とるべき方法であり、毎年補正予算を組むという

やり方は信頼性がない。

また、債務について総債務を見るべきか純債務を見るべきかという点であるが、良い

単一の数字はない。たとえば、見かけ上は債務水準が非常に低い国でも、年金制度が基

本的に均衡を欠いているために巨大な暗黙の負債を抱えていることがある。その国は債

務指標だけ見ると非常に良く見えるかもしれないが、SDSAを実施すると将来を見据

えた場合には事態は深刻であることがわかるだろう。したがって、そうした情報すべて

を一つの数字に還元することはできない。ある目的には純債務が有用であり、別の目的

には総債務が有用である。中央銀行が保有する政府債務は中央銀行にあるが、中央銀行

8

令和8年第3回経済財政諮問会議

にも負債がある。よって、統合的な見方は有益だが、単一の数字に依拠することはでき

ない。

自動安定化装置についてだが、私は以前からこれを推進してきた。ここには一貫性の

欠如がある。つまり、現に既存の仕組みは受け入れている。不況時に失業給付が増え、

税収が減り、自然に赤字が拡大することを、私たちは当然のように受け入れている。し

かしそれは、最初から設計されたものではなく、単にそうなっているというだけであ

る。そこで問われることは、もっと良くできないのかというのが問題である。実際私

は、経済状況に応じて自動的に発動される付加価値税率という考え方に取り組んでき

た。これは考える価値のある方向だと思うし、十分に使い得ると思う。

それが自動的であることは、十分にうまく設計されていれば、投資家にとって安心材

料になる。景気の良い時にも悪い時にも機能し、うまく設計されていれば、景気変動を

吸収しつつ債務増加につながらないからである。ただし、現在の日本には構造調整が必

要である。その意味で、今の優先課題は、1年や2年だけ付加価値税を下げることでは

なく、構造調整を行うことだと私は思う。不況であれば意味がある。しかし、今はそう

いう状況ではない。よって、「検討し、準備はしておくべき」だが、今日私が推したい

プログラムの一部ではないと申し上げたいと思う。

(ロゴフ氏) 多岐にわたるご意見やご質問、誠にありがとうございます。まず、市場

が信頼を失いつつある際に何に注目すべきかという総理のご質問から始めたいと思う。

もちろん、金利は最も分かりやすい指標だが、日本国債はいまだに、最も安全とまで

は言わないにしても、それに近いほど安全な国債と見なされていることを強調しておき

たいと思う。これは非常に価値のあること。もしその地位を失えば、日本の債務水準の

高さを考えれば、信認を喪失し金利が1パーセント上昇するだけで非常に痛手となるだ

ろう。長年にわたり金融危機や債務危機を研究してきた者として言えば、残念なことに

市場は大抵、そんなに前もって警告を発したりはしない。後になって振り返り、「あの

時に何か手を打っておくべきだった」と後悔することになる。それは一部には、政府が

情報を隠そうとしたり、手遅れになるまで市場に問題が見えないようにしようとしたり

するからでもある。

ブランシャール教授の述べた政府債務残高対GDP比に魔法の数字はないという点に

同意する。しかし、高い数字が望ましいものではないという点でも我々の意見は一致す

るだろう。高債務は国の強靱性を損ない、大きなショックへの対応をより慎重なものに

せざるを得なくする。多額の債務を抱える状態で金利が上昇すれば、それは痛みを伴

う。米国でも、フランスでも、日本でも、世界金利の上昇は痛みを伴う。それは調整の

一環であり、必ずしも政策運営を誤っていることを意味するわけではない。

私は、総理が計画しておられるように、成長を活性化し、これまでと異なるアプロー

チを模索するために一定のリスクを取ることには価値があると思う。日本は長年にわた

り安定的にはやってきたが、過去 30 年を見れば、本来もっと良くできたはず。

投資家が何を見るかについて一つの目安を挙げるとすれば、ブランシャール教授が強

調されたプライマリーバランスであり、それをどう回復していくかの計画である。私が

少し意見を異にするかもしれないのは、5年でそこへ到達すると約束すれば十分だ、と

いう点である。政治の言葉で5年後と言うのは、今のところ本気でそれをやるつもりは

ないと言っているのに近いもので、それでは実現しないおそれがある。将来の財政赤字

のことは、誰か他の人が頭を悩ませればよいという話になってしまいかねない。

9

令和8年第3回経済財政諮問会議

また、世界がより不安定になっている点も強調したいと思う。ブランシャール教授

は、金利と経済成長率の比較を重視している。これは実際に重要で、プライマリーバラ

ンスがゼロのとき債務がどう動くかを示すからだ。しかし、私たちは、成長も金利も急

に変わり得る、非常に不安定な世界に生きている。(課税の一形態である)金融抑圧と

いう手段で金利を人為的に低く抑えることはできるが、それも容易なことではない。

支出や政策をどこに集中すべきかという点では、もちろんロボティクスは日本が強み

を持ち、しかも成長している分野である。軍事研究もまた重要である。かつて米国のミ

サイル、たとえばパトリオットミサイルの中を開けると、多くの部品に日本語が書かれ

ていたものだ。それだけ多くの部品が日本製だったからである。今も多くの分野でそう

だが、以前ほどではないかもしれない。軍事支出は世界的な需要が大きいだけでなく、

イノベーションを促進する。米国では軍事支出が多くのイノベーションの最前線にあ

り、それが産業政策になっている。ある意味で、総理が提唱しておられる成長・イノベ

ーション活性化の考え方は、日本や欧州ではそれが十分に存在しなかったため、その代

替をしようとするものでもある。

他にも多くの質問を頂いたが、ドルに関する質問で締めくくる。私は、ドルの支配的

地位はこの10年ほど、実際に徐々に低下している状況にあると考えている。そして日本

も、将来、(インターネットや電子機器でどの標準を採用するかといった問題と同じよ

うな形で)ドルをめぐる問題にも直面するかもしれない。しかし、日本はその点で非常

に強い立場にあると思う。安全通貨の一つと見なされ続ける限り、日本はドル支配の漸

進的な後退から恩恵を得る可能性がある。そのためには、銀行システムや関連インフラ

の更新が必要かもしれない。日本のインフラの多くがそうであるように、銀行システム

もかなり古くなっているからである。しかし、そうした更新が進めば、長期的には日本

に大きな恩恵をもたらす可能性があり、将来の可能性も大いに開けると思う。ありがと

うございました。

(城内議員) 最後にブランシャール教授、ロゴフ教授から、高市政権に期待すること

をまとめていただくようお願いする。

(ブランシャール氏) 総理がお考えのことはきわめて実行可能だと思う。総理が提案

していることと、私が実行すべきと申し上げたこととの間にあまり違いはないと感じて

いる。信認は、一部には制度から生まれるとともに、投資家が総理の言うことと数字を

信頼できるかどうかにかかっている。信頼できる制度を整えることが極めて重要であ

る。そして最後に、総理の計画に敬意を表したいと思う。

(ロゴフ氏) ブランシャール教授が、非常に良いアイデアが示されていると述べた点

に、私も大いに賛同する。そして、当然ながら、実行が全てである。先ほど報道陣の前

でも申し上げたように、日本経済を活性化しようとする総理の努力に私は強く拍手を送

りたいと思う。

制度面で一つだけ選ぶとすれば、それは中央銀行の独立性が尊重されることを確実に

することである。これは理論上の話ではない。投資家がこれ以上に気にすることはな

い。私は世界中の人々と話しているが、米国で法の支配や関税など、さまざまな不安定

要因があるなかで、投資家が最も気にしているのはFRBは独立しているのかという点

である。日本でも同じだと思う。

10

令和8年第3回経済財政諮問会議

確かに財政制度は重要であるし、有望な政策案も数多く見られる。投資家が、総理が

中央銀行の独立性を守る姿勢を見て取れば、投資家は信認を高め、問題の発生を防ぐこ

とにつながるだろう。

本日はお招きいただき誠にありがとうございました。次の機会には、ぜひ直接お目に

かかれればと思う。

(城内議員) 最後に、高市総理からご挨拶を頂戴する。

(高市議長) 本日は、ブランシャール教授、ロゴフ教授のお二人をお迎えして活発な

ご議論をいただいた。特にロゴフ教授におかれては、そちらは早朝だと思うのだが、ご

参加いただき本当にありがとうございました。

お二人からは、「債務残高対GDP比」の安定化が欠かせないこと、また、ご意見は

多少食い違ったが、プライマリーバランスは5年程度で均衡を見る。違ったご意見も伺

った。公的投資の予算は「別枠管理」をしていくことの重要性、独立した予測を出す財

政機関に関するご提言、また、日本の強みを生かす分野への取組に着手することに対す

る評価、ドル中心の秩序からの変化の見通し、そして、お二人共通しているのだが、金

利上昇のリスクに備えた「リスク管理」の重要性など、たくさんのご示唆をいただい

た。

本日の議論も踏まえ、「責任ある積極財政」の具体化に向けた検討を加速したいと思

う。

先日10日の日本成長戦略会議でも申し上げたとおり、成長戦略と経済財政運営は一体

で進める必要がある。経済財政諮問会議においても、その実現に向けた議論を深めてい

ただきたいと思っている。

本会合に海外からも参加をいただき、貴重なご助言をいただいたお二人に改めて感謝

を申し上げる。

(城内議員) 以上をもって、本日の会議を終了する。

ブランシャール教授、ロゴフ教授、本当にありがとうございました。

(以 上)

11

令和8年第3回経済財政諮問会議

資料1

経済財政諮問会議(令和8年第3回)議事次第

令和8年3月26日(木)

18時00分~18時45分

総理大臣官邸4階大会議室

1. 開 会

2. 議 事

(1)

特別セッション

3. 閉 会

(資料)

資料1-1

資料1-2

資料2-1

資料2-2

オリヴィエ・ブランシャール氏提出資料(英語)

オリヴィエ・ブランシャール氏提出資料(事務局による日本語訳)

ケネス・ロゴフ氏提出資料(英語)

ケネス・ロゴフ氏提出資料(事務局による日本語訳)

配付資料1-1 現時点における高市政権の取組(内閣府)

配付資料1-2 現時点における高市政権の取組(内閣府)(事務局による英語訳)

資料2

資料1-1

Japanese Fiscal Policy: The Path forward

Olivier Blanchard

March 26, 2026

1/8

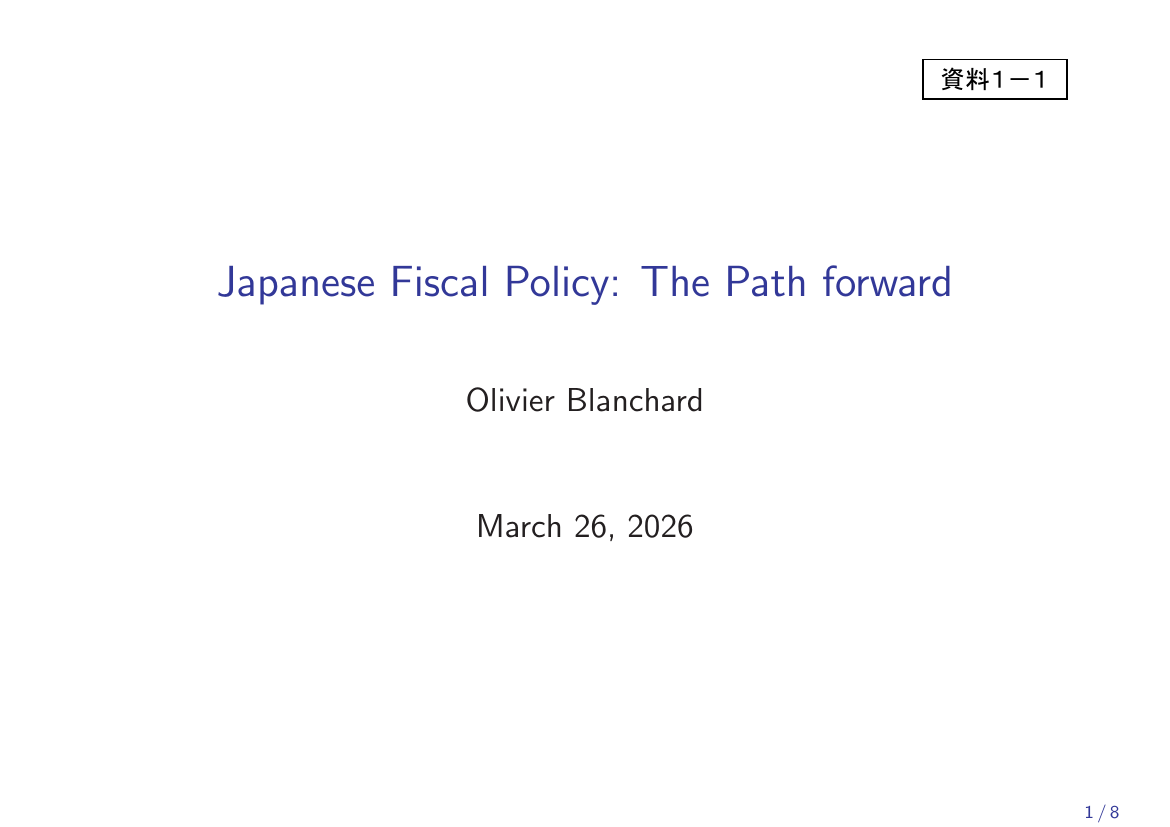

History: Primary Deficits and the Increase in Debt

Net debt ratio: from 20% in 1990 to about 130% today

Why the large rise? Two distinct reasons:

Low growth, political constraints, and optimistic forecasts

Sustaining weak private demand, monetary policy at the ZLB

Less of an issue now? End of secular stagnation? Likely, but

not certain.

2/8

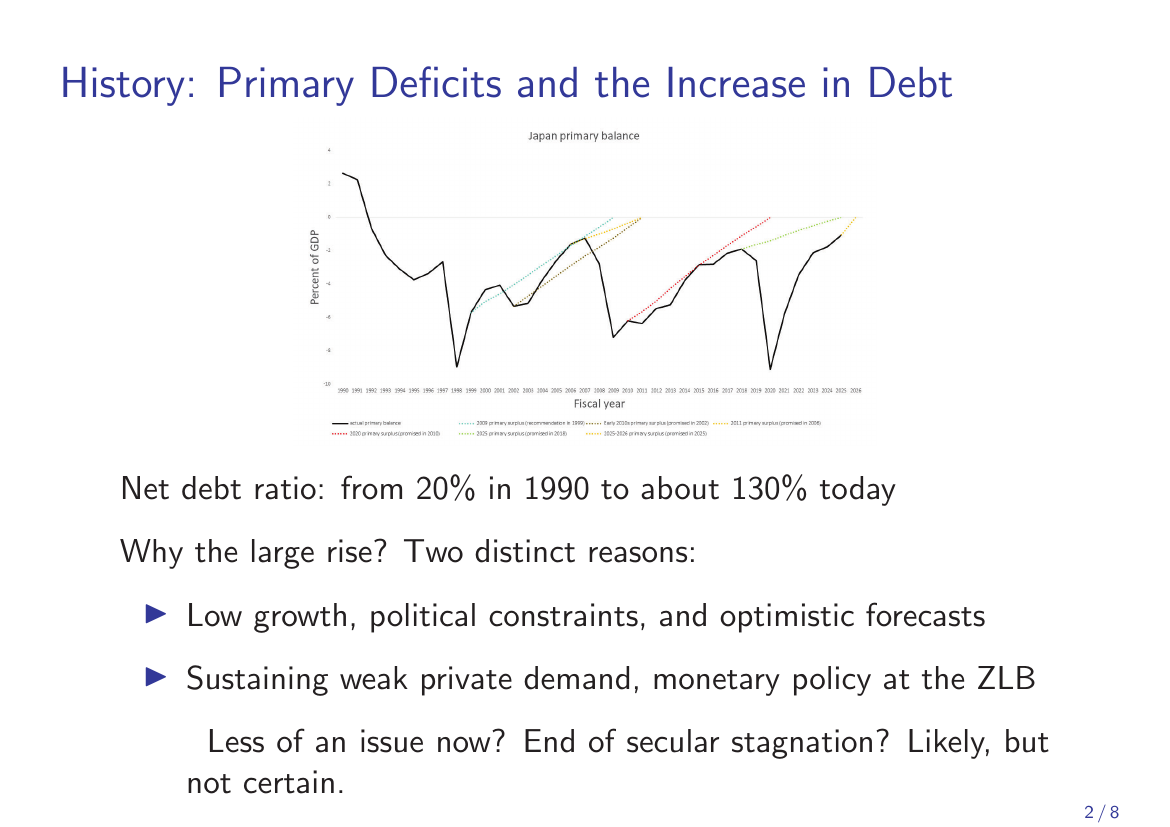

How much to worry about a high but stable debt ratio?

Depends fundamentally on (r − g )

If (r − g ) > 0 (standard textbook):

Welfare: Displacement of capital in portfolios; lower output later

Dynamics: Debt ratio increases even if primary deficit equals

zero

Need a primary surplus to stabilize debt ⇒ higher taxes

If (r − g ) < 0:

Welfare: Displacement not very costly (“dynamic inefficiency”

result)

Dynamics: Debt ratio decreases on its own, with zero primary

deficit

Can afford a (limited) primary deficit and still stabilize the debt

ratio

But: Even if (r − g ) < 0: amplification of (r − g ) uncertainty.

Dynamics depend on (r − g ) × b

3/8

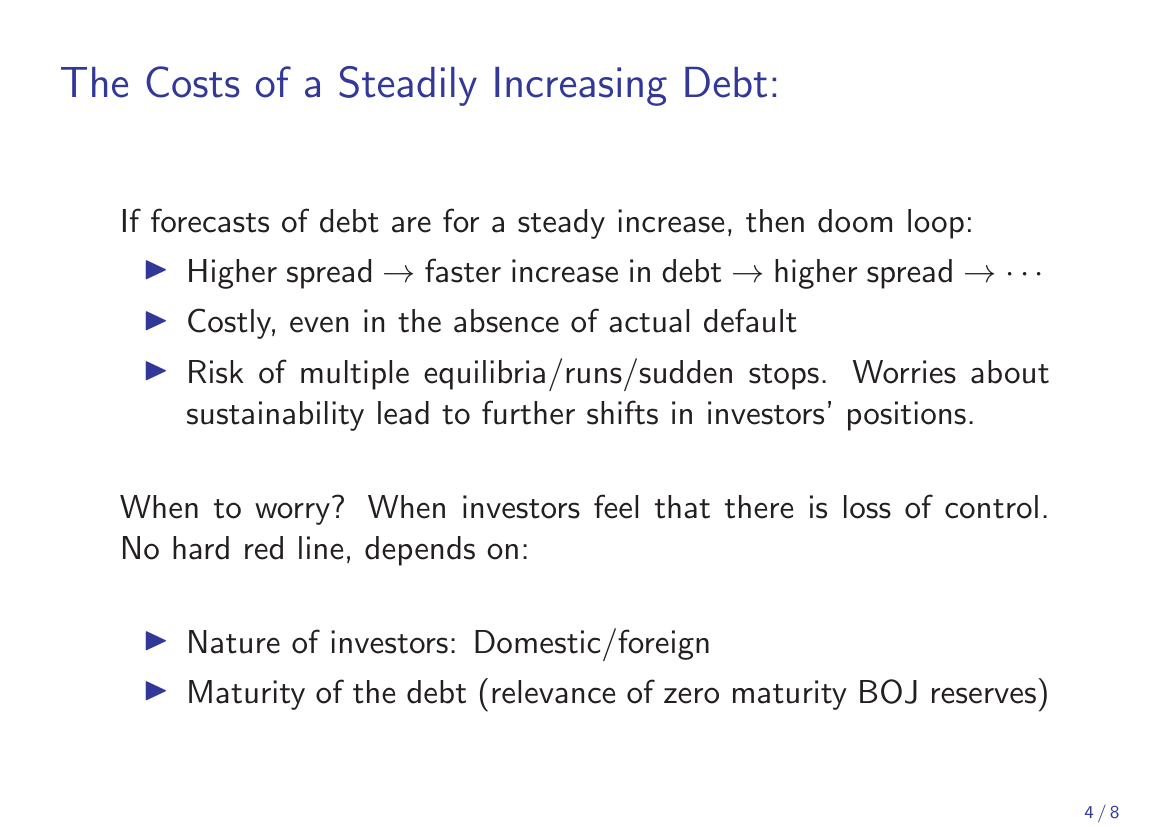

The Costs of a Steadily Increasing Debt:

If forecasts of debt are for a steady increase, then doom loop:

Higher spread → faster increase in debt → higher spread → · · ·

Costly, even in the absence of actual default

Risk of multiple equilibria/runs/sudden stops. Worries about

sustainability lead to further shifts in investors’ positions.

When to worry? When investors feel that there is loss of control.

No hard red line, depends on:

Nature of investors: Domestic/foreign

Maturity of the debt (relevance of zero maturity BOJ reserves)

4/8

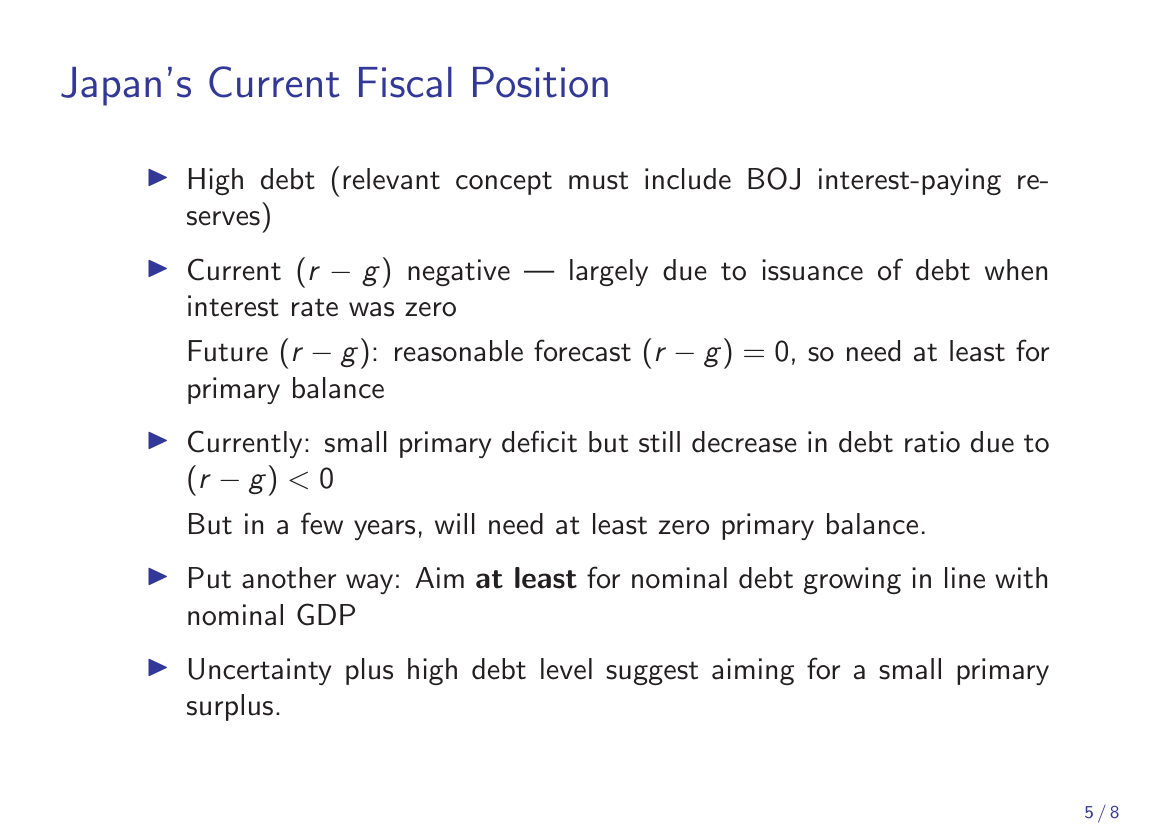

Japan’s Current Fiscal Position

High debt (relevant concept must include BOJ interest-paying reserves)

Current (r − g ) negative — largely due to issuance of debt when

interest rate was zero

Future (r − g ): reasonable forecast (r − g ) = 0, so need at least for

primary balance

Currently: small primary deficit but still decrease in debt ratio due to

(r − g ) < 0

But in a few years, will need at least zero primary balance.

Put another way: Aim at least for nominal debt growing in line with

nominal GDP

Uncertainty plus high debt level suggest aiming for a small primary

surplus.

5/8

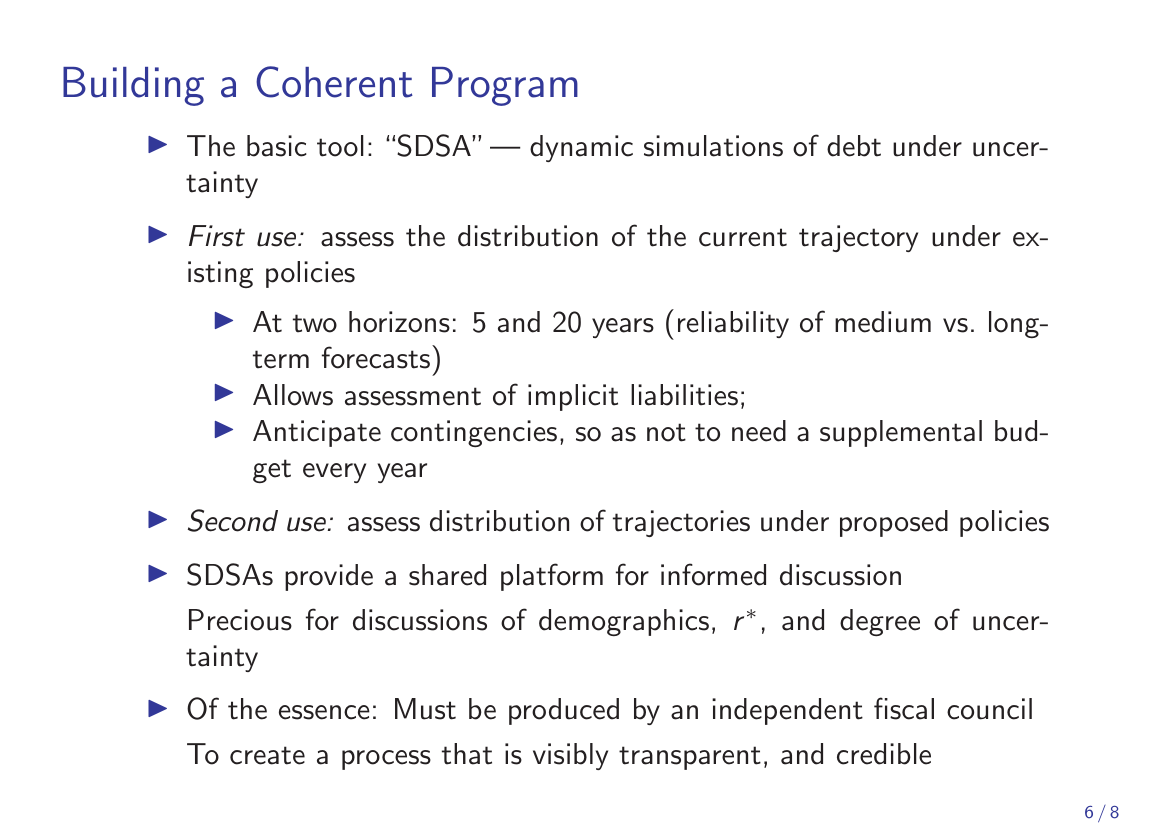

Building a Coherent Program

The basic tool: “SDSA” — dynamic simulations of debt under uncertainty

First use: assess the distribution of the current trajectory under existing policies

At two horizons: 5 and 20 years (reliability of medium vs. longterm forecasts)

Allows assessment of implicit liabilities;

Anticipate contingencies, so as not to need a supplemental budget every year

Second use: assess distribution of trajectories under proposed policies

SDSAs provide a shared platform for informed discussion

Precious for discussions of demographics, r ∗ , and degree of uncertainty

Of the essence: Must be produced by an independent fiscal council

To create a process that is visibly transparent, and credible

6/8

Implementation

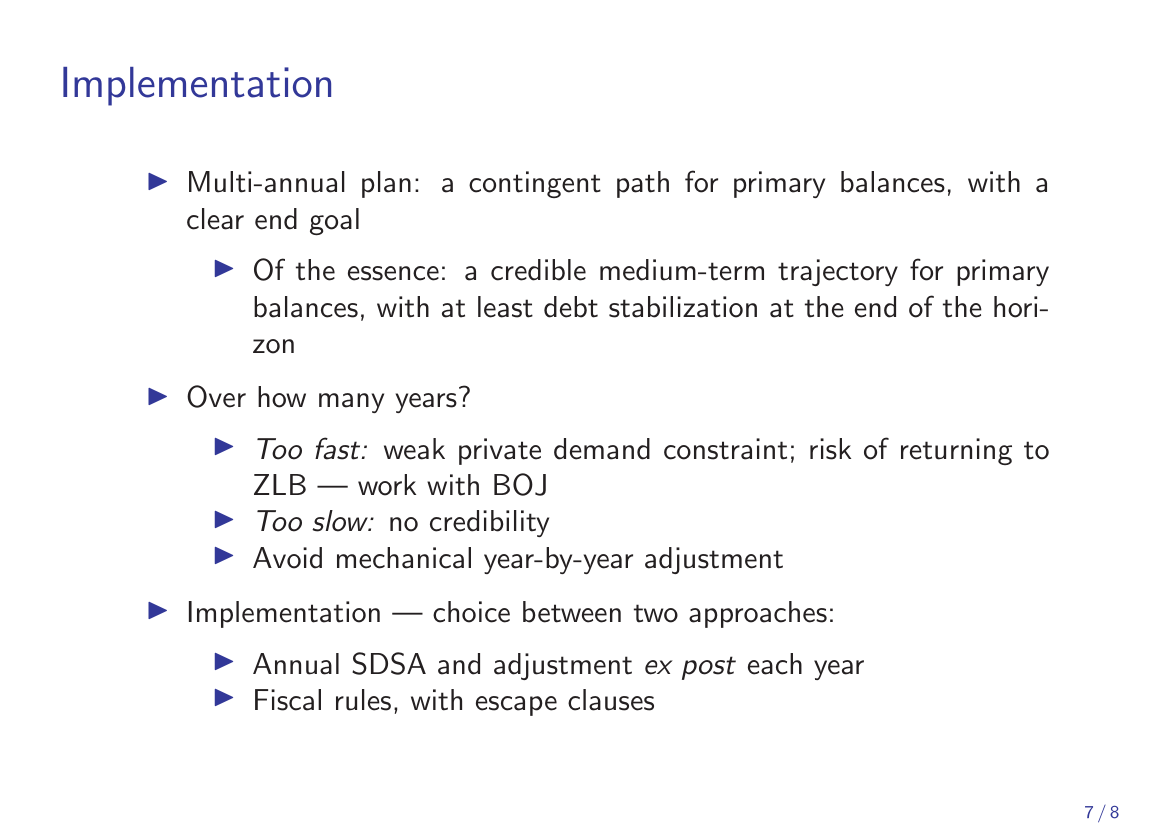

Multi-annual plan: a contingent path for primary balances, with a

clear end goal

Of the essence: a credible medium-term trajectory for primary

balances, with at least debt stabilization at the end of the horizon

Over how many years?

Too fast: weak private demand constraint; risk of returning to

ZLB — work with BOJ

Too slow: no credibility

Avoid mechanical year-by-year adjustment

Implementation — choice between two approaches:

Annual SDSA and adjustment ex post each year

Fiscal rules, with escape clauses

7/8

Public Investment

Should not get an automatic pass to be financed by debt

Most needed public investment does not generate enough future fiscal

revenues:

Defense, global warming

Reform-induced investments with uncertain returns: education,

research

“Strategic investments that enhance resilience against potential

crises”

SDSA is the right tool to assess the effect on the evolution of the

debt distribution

Still, if investment is urgent and required increase in taxation cannot

happen immediately:

Accept a temporary increase (or smaller temporary decrease) in the

primary deficit, so long as it preserves eventual debt stabilization

Need for transparency: separate investment account, with spending

and likely revenues

8/8

資料3

資料1-2

仮訳

日本の財政政策:今後の道筋

オリヴィエ・ブランシャール

2026年3月26日

※和訳資料は便宜的に作成したものであり、引用に当たっては英語版の資料1-1を利用ください。

1

歴史:プライマリーバランスの赤字と政府債務の増加

日本のプライマリーバランス

4

GDP比(%)

2

0

-2

-4

-6

-8

2026

2025

2024

2023

2022

2021

2020

2019

2018

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

-10

年度

実際のプライマリーバランス

2009年黒字化(1999年の提言)

2010年代初頭の黒字化(2002 年の目標)

2011年黒字化(2006年の目標)

2020年黒字化(2010年の目標)

2025年黒字化(2018年の目標)

2025年-2026年黒字化(2025年の目標)

政府純債務残高の対GDP比:1990年の20%から現在は約130%へ。

なぜ大幅に上昇したのか?二つの異なる理由:

低成長、政治的制約、楽観的な予測。

民間需要の低迷持続、金融政策のゼロ金利制約。

現在は問題が軽減?長期停滞の終焉?可能性はあるが、確実ではない。

2

高水準だが安定している政府債務残高対GDP比を、

どこまで懸念すべきか?

基本的に(r−g、金利−経済成長率)に依存する

(r−g) > 0(金利が経済成長率より大きい場合)(教科書的な場合):

厚生面:ポートフォリオにおける資本の置き換え;将来的な生産の低下。

動学面:プライマリーバランスの均衡でも政府債務残高対GDP比が上昇。

債務の安定にはプライマリーバランスの黒字が必要 ⇒ 増税

(r−g) < 0(経済成長率が金利よりも大きい場合):

厚生面:資本の置き換えのコストはさほど大きいものではない(「動学

的非効率性」の結果)。

動学面:プライマリーバランスの赤字がゼロでも政府債務残高対GDP比は

自然に低下。

(一定の)プライマリーバランスの赤字を許容しても政府債務残高対GDP

比を安定化させることが可能。

ただし:(r−g) < 0 であっても、(r−g)の不確実性は増幅される。政府債務

残高対GDP比の動きは (r−g) × b(bは政府債務残高対GDP比)に依存する。

3

着実に増加する債務のコスト

政府債務残高対GDP比の見通しが今後も着実に上昇し続けるものとなっている

場合、負の連鎖が起こり得る:

スプレッド上昇 → 政府債務残高対GDP比上昇の加速 → さらにスプレッ

ド上昇 →···

実際にはデフォルトが起きなくても、コストは大きい。

複数均衡/取り付け/急激な資本流出のリスク。財政の持続可能性への

懸念が、投資家のポジション調整をさらに促す。

懸念すべきタイミングは?投資家がコントロール喪失を感じた時。

明確な境界線はなく、以下の要素に依存:

投資家の性質:国内/海外

債務の満期構成(満期ゼロである日銀当座預金も関係する論点)

4

日本の現在の財政状況

債務水準は高い(関連して、付利のある日銀当座預金も含める必要)。

現在の(r-g)はマイナス(つまり、経済成長率が金利を上回る)。主な

要因として、ゼロ金利時に発行した国債が多いことによる。

将来の(r−g)は、合理的な予測として(r−g)=0 ⇒

イマリーバランスの均衡が必要。

少なくともプラ

現状:プライマリーバランスは小幅赤字だが、(r−g)<0のため政府債

務残高対GDP比は低下している。

ただし数年後には、少なくともプライマリーバランスの均衡が必要にな

る

言い換えれば:少なくとも、名目債務の伸びを名目GDPの伸びと同程度に

抑えることを、最低限の目標とする。

その上で、不確実性と高水準の政府債務残高対GDP比を踏まえると、多少

のプライマリーバランスの黒字を視野に入れることが示唆される。

5

整合的なプログラムの構築

基本ツール:「SDSA」ー不確実性の下での債務の動的シミュレーション

第一の用途:現行政策の下での財政経路の分布の評価。

2つの期間:5年と20年の見通し(中期見通しと長期見通しの信頼

性が異なるため)。

暗黙の負債の評価も可能。

想定外の事象を事前に織り込み、毎年の補正予算に頼らない設計に。

第二の用途:提案された政策の下での財政経路の分布の評価。

SDSAは、情報に基づく議論のための共通の基盤を提供する。

人口動態、r*(中立金利)、不確実性の度合い等に関する議論に有益。

最重要点:SDSAは独立した財政機関が作成すべきもの。

外から見ても透明で、信認できるプロセスを構築するという趣旨。

6

実装

複数年計画:プライマリーバランスの条件付き経路を示し、明確な最終

目標を置く。

最重要点:信頼に足る中期のプライマリーバランスの経路を提示し、計

画期間の末には少なくとも政府債務残高対GDP比の安定化を達成する。

何年かけて達成するか?

速すぎると:民間需要が弱いという制約があり、ゼロ金利制約に戻る

リスク――日銀との連携が必要。

遅すぎると:信認が得られない。

年々の機械的な調整を避ける。

実装ー2つのアプローチからの選択:

毎年SDSAを実施し、年次で事後的に調整。

例外条項を備えた財政ルール。

7

公的な投資

公的な投資だからといって、国債を財源とした実施が自動的に正当化さ

れるわけではない。

必要とされる公的な投資の多くは将来の歳入を十分には生まない:

防衛、地球温暖化対策

改革に伴うリターンが不確実な投資:教育、研究

危機管理投資

債務経路の分布の変化の評価には、SDSAが適切なツールである。

ただし、投資が急務であり、必要な増税を直ちに実施できない場合に

は:

最終的な債務の安定性を保つ限り、プライマリーバランスの赤字の一

時的な拡大(またはプライマリーバランスの赤字の改善ペースの一時

的な鈍化)を許容し得る。

透明性が不可欠:投資を別枠で区分管理し、歳出と見込まれる将来の歳

入を明示する。

8

資料4

資料2-1

Japan in a Higher-Rate World

Council on Economic and Fiscal Policy

Government of Japan

March 26, 2026

Kenneth Rogoff, Harvard University

1

The post-crisis low-rate world was the

exception for the global economy

• The global economy has moved away from the deflationary,

ultra-low-rate, low-inflation world that followed the 2007–08

financial crisis through the pandemic.

• Japan is not immune to the higher global rate environment.

• Long-term rates in Japan are more likely to rise than fall,

potentially reaching 3% over the coming decade.

• The forces pushing rates higher — debt, populism,

geopolitical fragmentation, military spending, and AIrelated investment — are likely to prove stronger than the

forces that have been pushing them lower, including

inequality, demography and low productivity growth.

2

The low-rate world is fading

3

Where Japan can build

• Markets are constantly being reshaped, so Japan should

start from areas where it already has real strengths.

• That points especially to robotics and advanced

manufacturing.

• Energy is another such area, including a larger role for

nuclear power in the energy mix.

• Defense-related capabilities will also matter more in a more

dangerous world; on the plus side, military R&D often has

important civilian spillovers.

• The plan to make the government less reliant on

supplementary budgets would increase predictability and

thus help support both public and private investment.

4

Preparing for higher rates

• In a world of higher interest rates, Japan will need to

preserve room for the debt-to-GDP ratio to fall gently in

normal times (which seem to be happening less and less

often).

• That argues for keeping the primary deficit near balance

outside crises.

• Government debt is deeply embedded in the financial

system, so if rates rise too quickly, the challenge will be

financial as well as fiscal.

• Consumption tax relief may make sense in some

circumstances, but policymakers will need to be responsive

if interest rates rise sharply.

5

Global instability and a weakening of

dollar hegemony

• A major macroeconomic risk for Japan is growing instability

in the global economy, including uncertainty over policy in

the United States and other major economies.

• Alongside trade tensions, financial restrictions, and

geopolitical conflict, this could weaken the dollar-centered

system and hasten a shift toward a more multipolar order,

with the renminbi playing a larger role in Asia and the euro,

crypto assets, and gold gaining importance.

• For Japan, this raises a broader strategic question: whether

it is resilient to a less stable dollar-centered system.

6

Appendix:

Secular stagnation was the exception

7

資料5

資料2-2

仮訳

金利上昇局面の世界における日本

経済財政諮問会議

2026年3月26日

ハーバード大学

ケネス・ロゴフ

※和訳資料は便宜的に作成したものであり、引用に当たっては英語版の資料2-1を利用ください。

1

金融危機後の低金利環境は例外だった

• 世界経済は、2007年から2008年の金融危機後からパン

デミック期まで続いた、デフレ的で超低金利・低イン

フレの世界から離れつつある。

• 日本も世界的な金利上昇の環境から免れることはでき

ない。

• 日本の長期金利は下落するよりも上昇する可能性が高

いとみられ、次の10年のうちには長期金利が3%に達す

る可能性もある。

• 債務、ポピュリズム、地政学的分断、軍事支出、AI関

連投資といった金利押上げ要因は、格差、人口動態、

生産性低迷といったこれまで金利を押し下げてきた要

因よりも強い影響力を持つことになるだろう。

2

低金利時代が終わりを告げつつある

米国10年物価連動国債の市場利回り

3

日本が強みを発揮できる分野

• 市場は絶えず変化している。したがって、日本はすで

に確かな強みを持つ分野から着手すべきである。

• とりわけ、ロボティクスや先端製造業がそれに当たる。

• エネルギー分野もその一つであり、エネルギーミック

スにおける原子力の役割拡大も含まれる。

• また、世界情勢がより危険なものとなる中、防衛関連

の能力も一層重要になるだろう。加えて、防衛分野の

研究開発は民生分野への波及を生むことも少なくない。

• 補正予算への依存度を低減させる政府の方針は、予見

可能性を高め、ひいては官民双方の投資を支えること

につながるだろう。

4

金利上昇への備え

• 金利上昇局面において、日本は平時に債務残高対GDP比

を緩やかに低下させていく余地を確保する必要がある

(もっとも、そうした平時はますます少なくなってい

るように見える)。

• そのためには、危機時を除き、プライマリーバランス

の赤字を概ね均衡に近い水準に保つことが求められる。

• 政府債務は金融システムに深く組み込まれているため、

金利が急上昇した場合、課題は財政面だけでなく金融

面にも及ぶことになる。

• 消費税負担の軽減は一定の場合において妥当なことは

ありうるが、金利が急上昇する局面では政策当局は機

動的に対応する必要がある。

5

世界の不安定化とドル覇権の弱体化

• 日本にとっての大きなマクロ経済リスクの一つは、米

国その他の主要国の政策をめぐる不確実性を含め、世

界経済の不安定化の進行である。

• 通商摩擦、金融的制限措置、地政学的対立が重なる中

で、こうした動きはドル中心の体制を弱体化させ、人

民元がアジアでより大きな役割を果たすとともに、

ユーロ、暗号資産、金の重要性も高まり、より多極的

な秩序への移行を加速させる可能性がある。

• 日本にとっては、これはより大きな戦略的問いを提起

している。すなわち、安定性を失っていくドル中心の

体制に対して、日本は十分な強靱性を備えているかど

うかという点である。

6

付録:長期停滞こそが例外だった

パーセント

世界実質金利

世界実質金利:長期成分

長期停滞と

言われた時代

(出所)

7

資料6

配付資料1-1

現時点における高市政権の取組

2026 年3月

内閣府

基本認識

日本は技術革新力・労働の効率性という底力があるのに、国内投資が不足し、潜在成長率が低迷してい

る

「過度な緊縮志向」

「未来への投資不足」から完全に脱却し、国が一歩前に出て投資を呼び込む

危機管理投資、成長投資

危機管理投資:経済安全保障/食料・エネルギー/国土強靱化/医療・防災/サイバー等、リスク最小

化

成長投資:研究開発・人材・先端分野、AI、スタートアップ、量産・社会実装、海外展開

官民協調で戦略的に国内投資を大胆に促進し、雇用・所得・生産性を引き上げる

予算編成の在り方の見直し/財政ルール

民間事業者や地方自治体の取組を後押しするため、政府予算の予見可能性を確保する観点から、毎年度

補正予算が組まれることを前提とした予算編成と決別し、可能な限り当初予算で措置するなど、予算の

作り方を抜本的に見直し

(例)必要な財源を確保しながら措置する複数年度予算や長期的な基金による投資促進策

予算のメリハリ付け等を通じて、財政の持続可能性を確保

(例)租税特別措置・補助金見直し担当室の設置などの行財政改革等

政府債務残高の対GDP比の安定的な引下げに向けて、具体的な指標を明確化

家計支援

飲食料品に限った2年間の消費税引下げ

給付付き税額控除の導入:必要な層に厚く、家計支援の精度を上げる

アベノミクスとの違い

アベノミクスは、

「3本の矢」

(金融緩和・機動的な財政・成長戦略)でデフレ脱却と需要喚起に重点

いわゆるサナエノミクスは「責任ある積極財政」として、官民協調で戦略的に国内投資を大胆に促し、

供給力(潜在成長)を上げ、投資と成長の好循環を促す

(出典)

・施政方針演説(第 221 回国会)

、経済演説(第 221 回国会)

、経済財政諮問会議の資料

資料7

配付資料1-2

The Takaichi administration's economic and fiscal policies

March 2026

Cabinet Office

Basic Diagnosis

Japan has strong underlying strengths—high technological innovation capabilities and the

efficiency of labor —yet domestic investment has been insufficient, and the potential growth

rate is declining.

Japan must sever the trends of excessive austerity and underinvestment in the future; the

government should step forward to catalyze private investment.

Crisis Management Investments and Growth Investments

Crisis-Management Investments: minimize strategic risks through targeted investment in

economic security; food, energy and critical resources; national resilience; health and

disaster preparedness; cybersecurity; and related areas.

Growth Investments: scale up investment in R&D, talent, frontier technologies, AI, startups,

mass production and social implementation, and global market expansion.

Through public–private coordination, boldly boost domestic investment strategically and

increase employment, income, and productivity.

Reforming the Budget Framework/ Fiscal Rules

To support efforts taken by both private-sector entities and local governments, and with a

view to ensuring the predictability of government budgets, we will fundamentally overhaul

the way the national budget is created, such as by making a clean break from our current

budget formulation process in which it is assumed that a supplementary budget will be

compiled each fiscal year, and instead allocating all necessary funds within the initial

budget, to the extent possible.

(Example)Investment promotion measures through fiscal outlays across multiple fiscal

years with securing of necessary resources, and funding that is provided over the long

term.

Ensure fiscal sustainability through strategic choices across the budget

(Example)Administrative and fiscal reform, including establishment of an Office for the

Review of Special Measures Concerning Taxation and Subsidies

Make clear indicators for steadily reducing the government debt-to-GDP ratio.

Household Support

A suspension of the consumption tax, which is limited to food and beverage items and only

for a period of two years.

Introduction of a refundable tax credit system: concentrate support on those who need it

most and improve the precision of household assistance.

1

How It Differs from Abenomics

Abenomics, the “three arrows” (bold monetary policy, flexible fiscal policy, and growth

strategy), focused on exiting deflation and stimulating demand.

So-called Sanaenomics, centered on “responsible and proactive public finances,” with:

• Boldly promote domestic investment strategically through public–private

coordination, raise supply capacity (higher potential growth) , and generate a

virtuous cycle of investment and growth.

Sources: Policy Speech by the Prime Minister (221st Session of the Diet), Economic Policy

Speech (221st Session of the Diet), Materials from the Council on Economic and

Fiscal Policy

2